Read More

"To Persist or not to Persist, that is the question." At the heart of every asset manager's morning routine lies a deceptively simple problem: whose numbers do you trust when the market opens? Do you preserve your OMS positions and let the system update itself, or do you wipe the slate clean each morning and reload from an independent source? Two distinct philosophies have emerged to answer this — and the choice says a lot about how a firm thinks about risk, control, and operational resilience.

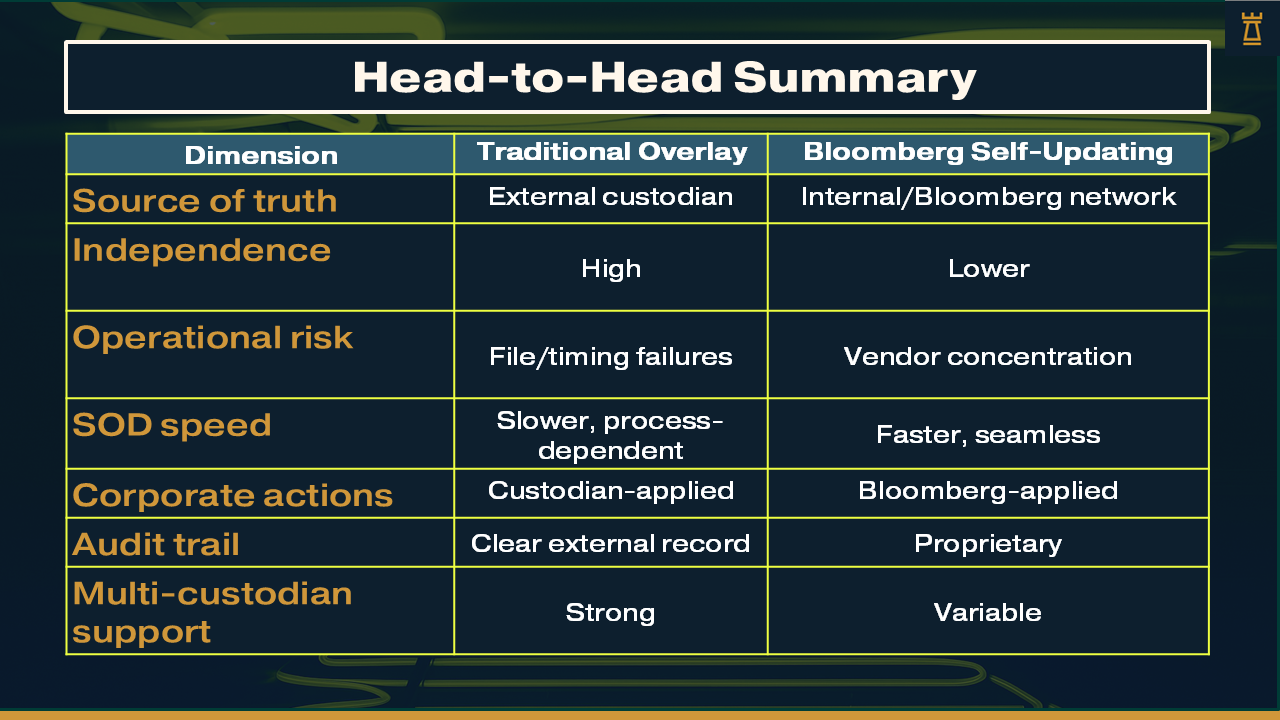

Most asset managers begin their day by pulling "golden copy" position data from their Middle Office or Custodian and overlaying it onto their Order Management System (OMS). In practical terms, this means the OMS is treated as an intraday working tool only — its positions at end of day are essentially discarded or set aside, and the authoritative numbers from the custodian (who has settled, reconciled, and confirmed all transactions against the actual assets held) are pushed back in each morning to reset the ledger.

The workflow typically looks like this: the custodian or middle office produces a settled position file overnight, that file is transmitted to the OMS via SFTP or an integration layer, and the portfolio managers and traders arrive in the morning to find positions that reflect actual settled holdings — complete with corporate actions, income events, and failed trade adjustments already incorporated.

Opinion: The overlay model exists for good reason. Custodians are the legal record-keepers of assets, and their data reflects what has actually settled at the depository level. Using them as the SOD source of truth adds a crucial independent check, catches OMS-side errors, and ensures the firm is trading on real economic exposure rather than an internally-derived number that may have drifted. The downside is significant operational fragility — the process involves file dependencies, timing risk, format mapping issues, and a reconciliation break investigation burden. On a bad morning, PMs can be locked out of meaningful decision-making until the overlay clears, which in volatile markets is genuinely costly.

Bloomberg AIM (and similar closed-ecosystem platforms) takes a fundamentally different approach. Rather than treating the OMS as a transient intraday tool, it maintains a continuous and self-updating position ledger. Bloomberg receives trade confirmations, settlement notifications, corporate action data, and pricing feeds directly and autonomously, applying them to positions without requiring a human-initiated overnight overlay. The system essentially reconciles itself on a rolling basis, so by the time users log in, the positions have already been updated through Bloomberg's own data network.

Opinion: This is an elegant model when it works, and for many firms it works very well. Bloomberg's data infrastructure is genuinely world-class, and the tight integration between their market data, corporate actions, and trade processing pipelines removes a huge amount of manual intervention. The SOD experience is smoother and faster. The concern, however, is one of dependency and trust — you are relying entirely on a single vendor's interpretation of settlement and corporate action events, with less visibility into how discrepancies are resolved. If Bloomberg has a data issue, you may not know until a break surfaces downstream. Firms with complex, multi-custodian, multi-asset structures may also find Bloomberg's self-reconciliation less comprehensive than a proper custodian-driven overlay. There's also a philosophical point: regulators and auditors tend to view custodian-sourced positions as the independent gold standard, and a self-referential system — however sophisticated — doesn't provide that same separation of duties.

The honest view is that neither model is strictly superior — the right answer depends on the firm's complexity, its tolerance for vendor dependency, and how mature its middle office infrastructure is. A large multi-asset manager running across a dozen custodians globally almost certainly needs the overlay discipline. A mid-sized long-only equity manager running a clean book in Bloomberg AIM may find the self-updating model perfectly adequate and operationally far simpler.

Salvadore Auditore

Managing Consultant

TorreBlanc